Caffeine hit: the politics and economics of the $5.08 coffee

"In 2024 and beyond, fee-free digital payments should be the norm, not an exception."

Introduction (the politics of the $5.08 coffee)

Labor MP Jerome Laxale brought a little bit of political theatre to Federal Parliament earlier this month, when he sought to shine a light on the surcharges which Australians pay on debit and credit card transactions.

Amidst a cost-of-living crisis these fees are hard to ignore. Repeatedly popping up as we tap our cards and mobile wallets.

As per the image below, Laxale used the example of a cup of coffee costing 8c more than the cash alternative, even when you are paying with a debit card.

In the House Economics Committee he had Australia’s bank bosses squirming in their seats as they sought to distil a complex value chain into:

Media-friendly sound bites

That would not appear like rent-seeking behaviour

The economics of the $5.08 coffee

In his coverage of the event AFR journalist James Eyres did his best to provide some transparency, going so far as to break down where the costs are coming from.

(However I’m not sure terms such as ‘interchange fee’, ‘scheme fee’ and ‘acquirer margin’ would leave his readers any the wiser).

The crux of the issue is twofold:

Payment platforms such as Square are bundling debit cards in with credit card transactions, leaving poor millennials to subsidise the generous frequent flyer rewards of all those boomers

That these transactions do not represent final settlement drives enormous costs into the system, even though the proportion of events that need to be revisited is measured in basis points (if that)

Taking a step back

Jerome’s debate that day was the monetary equivalent of splicing your three wood into the deep rough on the ninth. Once the ball goes in, you could spend hours without actually finding what you were looking for.

But if a Bitcoin policy advocate had been in the room that day, we might well have had a hole in one.

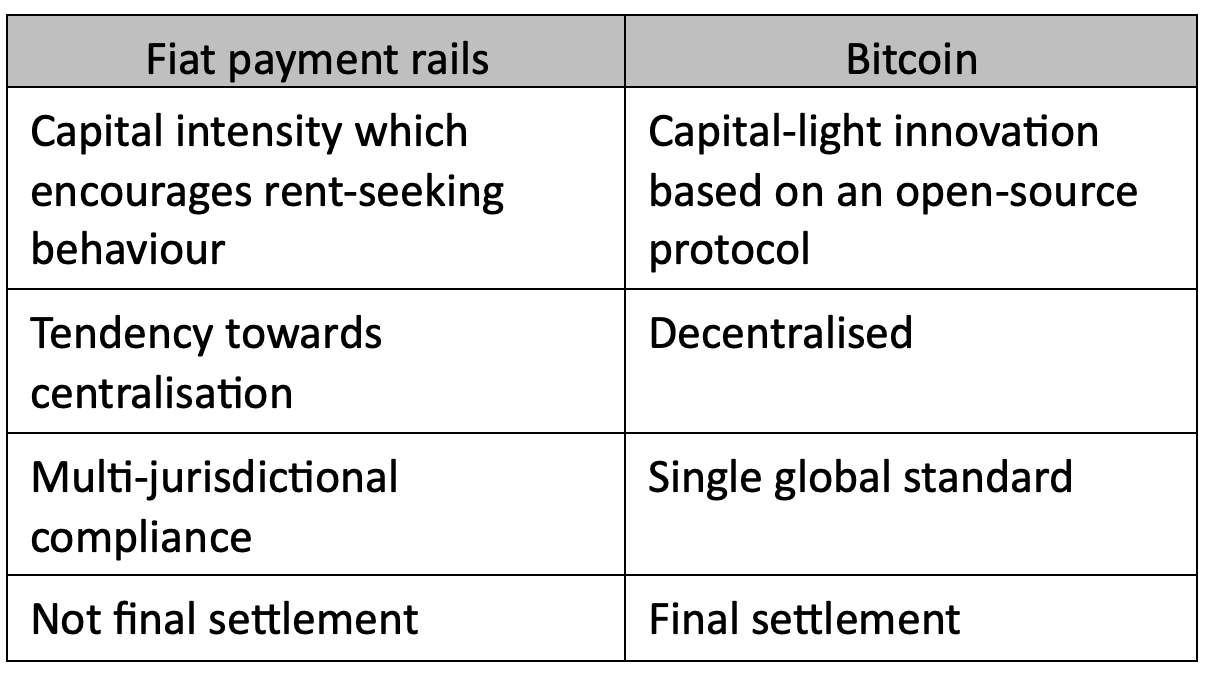

The following table (a comparison between our existing ‘fiat’ payment rails and Bitcoin) is an attempt to drive the conversation straight to the target, which as Jerome said is fee-free digital payments.

The economics of settlement

If (as the AFR quoted) we are spending $1 trillion a year across 15 billion transactions, then the average value is just $66 (and one can imagine the billions that are just a few dollars).

Under those circumstances it simply doesn’t make economic sense to apply the same settlement model to such a high volume of low value transactions.

(Are you really going to your bank for a refund when your favourite decaf, soy cappuccino is not up to scratch?)

Enter Bitcoin

And as always we end up with Bitcoin.

It is unfortunate that Jerome doesn’t have three arms.

Because if he did he could have held up:

The $5.08 debit card

The $5.00 note

Had he done so it would have shown all of the advantages of the Lightning network in one simple screen shot.

Conclusion

As Eyres commented in his article, “The Reserve Bank may be compelled to follow the UK and Europe and ban credit and debit card surcharges.”

The RBA is expected to release a consultation paper in the next few months.

If they do implement a ban it will force countless SMEs to:

Incorporate these costs into their default pricing model

While at the same time driving them to seek out lower cost payment channels

Either way this will be a classic opportunity to highlight the benefits of a future where fee-free, low value digital payments have indeed become the norm.